Is the Wall Street Cartel Regrouping? Regulator Fires Warning Shot By Pam Martens and Russ Martens:

| |

| April 28, 2016 |

Bethany Dugan, Deputy Comptroller for Operational Risk at the OCC

Well, apparently, one or more banks are causing concerns in this area again.

Yesterday, the regulator of national banks, the Office of the Comptroller of the Currency, sent out a severe warning to its flock that there could be a five year jail sentence waiting in the wings for anyone attempting to use technology to block its mandated access to bank records. The letter was authored by Bethany Dugan, Deputy Comptroller for Operational Risk. The statement read in part:

“The OCC has become aware of communications technology recently made available to banks that could prevent or impede OCC access to bank records through certain data deletion or encryption features.” Another part of the memo honed in on the chat room issue, noting that “…OCC is aware that some chat and messaging platforms have touted an ability to ‘guarantee’ the deletion of transmitted messages. The permanent deletion of internal communications, especially if occurring within a relatively short time frame, conflicts with OCC expectations of sound governance, compliance, and risk management practices as well as safety and soundness principles.”

Curiously, a footnote called out the Board and bank management of unnamed banks, suggesting that there has been a concerted effort to block the OCC examiners from access to chat rooms and/or to speak directly to bank staff:

“Failure to provide timely access, or

efforts by the board of directors or bank management to impede the bank

staff’s ability to provide such access, may result in enforcement

action. Furthermore, examination obstruction may subject individuals to

criminal prosecution. Refer to 18 USC 1517, ‘Obstructing Examination of

Financial Institution.’ ”

The statute referenced by the OCC, 18 USC 1517, is succinct and

harsh: “Whoever corruptly obstructs or attempts to obstruct any

examination of a financial institution by an agency of the United States

with jurisdiction to conduct an examination of such financial

institution shall be fined under this title, imprisoned not more than 5

years, or both.”Wall Street watchers are speculating that this may be another dustup over the communications system called Symphony that was initiated by Goldman Sachs. Goldman provides a detailed explanation on its web site about how it built out this system and admits that it got a “consortium” of other mega banks and hedge funds to join its plan. It also explains how it hired an expert in “encryption” to head it up, writing:

“In an effort to further develop and

evolve the platform, Goldman Sachs built a consortium of the world’s

leading financial services firms and acquired Perzo, a Palo Alto startup

led by David Gurle, an expert in encryption and security, to form

Symphony Communication Services Holdings LLC.”

In a press release

issued in 2014, Symphony said that its financial institution partners,

in addition to Goldman, included: Bank of America Merrill Lynch, BNY

Mellon, BlackRock, Citadel, Citigroup, Credit Suisse, Deutsche Bank,

Jefferies, JPMorgan, Maverick, Morgan Stanley, Nomura and Wells Fargo.”The New York State Department of Financial Services was sufficiently concerned about the encryption aspect of the Symphony platform that it reached an agreement with four of the banks that it regulates (Goldman Sachs, Deutsche Bank, Credit Suisse, and Bank of New York Mellon) in September of last year.

Anthony J. Albanese, Acting Superintendent of Financial Services, said at the time of the agreement: “We are pleased that these banks did the right thing by working cooperatively with us to help address our concerns about this new messaging platform. This is a critical issue since chats and other electronic records have provided key evidence in investigations of wrongdoing on Wall Street. It is vital that regulators act to ensure that these records do not fall into a digital black hole.”

Initially, Symphony was promoting its platform with a promise of “Guaranteed Data Deletion,” raising red flags among New York State regulators.

Under the agreement with the State of New York, the four banks agreed to retain a copy of all e-communications sent through the Symphony platform for seven years and store duplicate copies of the decryption keys for these communications with independent custodians not controlled by the banks. The other 10 financial firms partnering with Symphony were not, however, parties to the agreement.

The specific language in the agreement noted that the Symphony platform uses “end-to-end encryption” which “enables the transmission of encrypted messages – including chat and instant messages – where only the sender and recipient institutions can decrypt the message using a private decryption key, and Symphony does not have the ability to decrypt the message.”

Why the Vampire Squid Wants Small Depositors’ Money in 1 Frightening Chart

By Pam Martens and Russ Martens: April 27, 2016

Back in 2010, with the public still numb from the epic financial

crash and still in the dark about the trillions of dollars of secret

loans the Federal Reserve had pumped into the Wall Street mega banks to

resuscitate their sinking carcasses, Matt Taibbi penned his classic profile of Goldman Sachs at Rolling Stone,

with this, now legendary, summation: “The world’s most powerful

investment bank is a great vampire squid wrapped around the face of

humanity, relentlessly jamming its blood funnel into anything that

smells like money.”

Historically, what smells like money to Goldman Sachs has been eight-figure money and higher. As recently as 2013, the New York Times reported that Goldman had a $10 million minimum to manage private wealth and was kicking out its own employees’ brokerage accounts if they were less than $1 million. Now, all of a sudden, Goldman Sachs Bank USA is offering FDIC insured savings accounts with no minimums and certificates of deposits for as little as $500 with above-average yields, meaning it’s going after this money aggressively from the little guy. What could possibly go wrong?

The last utterances we ever hoped to see bundled into a bank promotion were the words “Goldman Sachs” and “FDIC insurance” and “peace-of-mind savings.” But that’s what now greets one at the new online presence of Goldman Sachs Bank USA, thanks to the repeal of the Glass-Steagall Act in 1999, which allowed high-risk investment banks like Goldman Sachs to also own FDIC-insured, deposit-taking banks.

Goldman Sachs has been paying lots of fines for wrongdoing in the past few years, topping off at a cool $5 billion earlier this month for what the U.S. Justice Department characterized as “serious misconduct in falsely assuring investors that securities it sold were backed by sound mortgages, when it knew that they were full of mortgages that were likely to fail.” There was also the $550 million settlement in 2010 with the SEC for Goldman allowing the hedge fund run by billionaire John Paulson to secretly assist it in creating a portfolio designed to fail so Paulson could short it, while Goldman sold it to its own clients without divulging this pesky detail.

Students of Wall Street history may also recall that Goldman’s hubris leading up to the crash of 1929 played a role in why the Glass-Steagall Act of 1933 banned casino-like investment banks from getting near insured deposits. Prior to the ’29 crash, Goldman ran the Goldman Sachs Trading Company, a closed end fund (called a trust in those days). Goldman Sachs also offered that deal to the little guy at $104 a share. The fund appeared to investigators as a dumping ground for Goldman while also paying it a hefty management fee. The little guy who bought the shares at $104 a share at the top of the bull market was left with about a buck and change after the ’29 crash.

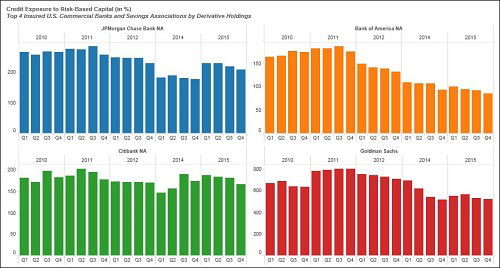

So why this generous move now by Goldman Sachs Bank USA to offer above average returns to the little guy? It likely has a lot to do with the chart below from the Office of the Comptroller of the Currency’s (OCC) December 31, 2015 report on the four largest banks based on derivatives exposure. According to the report, the credit exposure from derivatives versus the bank’s risk-based capital is as follows: JPMorgan Chase 209 percent; Bank of America 85 percent; Citibank 166 percent and Goldman Sachs (wait for it) – a whopping 516 percent.

Not to put too fine a point on it, but you might recall that one of the key promises of the Dodd-Frank financial reform legislation was that after the largest bank bailout in financial history in 2008, these derivatives were going to be pushed out of the insured bank into bank affiliates that would not endanger the taxpayer-backstopped deposits and force another monster taxpayer bailout in the next crisis. This became known as the “push-out rule” which could never seem to materialize into a hard and fast law. Then, in December 2014, Citigroup simply used its muscle to legislate the rule out of existence.

The Obama administration also promised that Dodd-Frank would put an end to these trillions of dollars of opaque derivatives being traded in the dark between firms as private contracts (over-the-counter). Dodd-Frank promised to bring them into the sunshine at central clearinghouses. But the December 2015 report from the OCC makes clear that’s just another failed promise, stating:

When you hear Hillary Clinton repeatedly tell the public that she wants to continue along the same pathways as President Obama and that the restoration of the Glass-Steagall Act is not needed, let the image of Goldman Sachs Bank USA and its FDIC insurance logo and its $41 trillion in derivatives come to mind.

Goldman Sach’s Advertising Slogan Is “Progress Is Everyone’s Business.”

Historically, what smells like money to Goldman Sachs has been eight-figure money and higher. As recently as 2013, the New York Times reported that Goldman had a $10 million minimum to manage private wealth and was kicking out its own employees’ brokerage accounts if they were less than $1 million. Now, all of a sudden, Goldman Sachs Bank USA is offering FDIC insured savings accounts with no minimums and certificates of deposits for as little as $500 with above-average yields, meaning it’s going after this money aggressively from the little guy. What could possibly go wrong?

The last utterances we ever hoped to see bundled into a bank promotion were the words “Goldman Sachs” and “FDIC insurance” and “peace-of-mind savings.” But that’s what now greets one at the new online presence of Goldman Sachs Bank USA, thanks to the repeal of the Glass-Steagall Act in 1999, which allowed high-risk investment banks like Goldman Sachs to also own FDIC-insured, deposit-taking banks.

Goldman Sachs has been paying lots of fines for wrongdoing in the past few years, topping off at a cool $5 billion earlier this month for what the U.S. Justice Department characterized as “serious misconduct in falsely assuring investors that securities it sold were backed by sound mortgages, when it knew that they were full of mortgages that were likely to fail.” There was also the $550 million settlement in 2010 with the SEC for Goldman allowing the hedge fund run by billionaire John Paulson to secretly assist it in creating a portfolio designed to fail so Paulson could short it, while Goldman sold it to its own clients without divulging this pesky detail.

Students of Wall Street history may also recall that Goldman’s hubris leading up to the crash of 1929 played a role in why the Glass-Steagall Act of 1933 banned casino-like investment banks from getting near insured deposits. Prior to the ’29 crash, Goldman ran the Goldman Sachs Trading Company, a closed end fund (called a trust in those days). Goldman Sachs also offered that deal to the little guy at $104 a share. The fund appeared to investigators as a dumping ground for Goldman while also paying it a hefty management fee. The little guy who bought the shares at $104 a share at the top of the bull market was left with about a buck and change after the ’29 crash.

So why this generous move now by Goldman Sachs Bank USA to offer above average returns to the little guy? It likely has a lot to do with the chart below from the Office of the Comptroller of the Currency’s (OCC) December 31, 2015 report on the four largest banks based on derivatives exposure. According to the report, the credit exposure from derivatives versus the bank’s risk-based capital is as follows: JPMorgan Chase 209 percent; Bank of America 85 percent; Citibank 166 percent and Goldman Sachs (wait for it) – a whopping 516 percent.

Not to put too fine a point on it, but you might recall that one of the key promises of the Dodd-Frank financial reform legislation was that after the largest bank bailout in financial history in 2008, these derivatives were going to be pushed out of the insured bank into bank affiliates that would not endanger the taxpayer-backstopped deposits and force another monster taxpayer bailout in the next crisis. This became known as the “push-out rule” which could never seem to materialize into a hard and fast law. Then, in December 2014, Citigroup simply used its muscle to legislate the rule out of existence.

The Obama administration also promised that Dodd-Frank would put an end to these trillions of dollars of opaque derivatives being traded in the dark between firms as private contracts (over-the-counter). Dodd-Frank promised to bring them into the sunshine at central clearinghouses. But the December 2015 report from the OCC makes clear that’s just another failed promise, stating:

“In the first quarter of 2015, banks

began reporting their volumes of cleared and non-cleared derivatives

transactions, as well as risk weights for counterparties in each of

these categories. In the fourth quarter of 2015, 36.9 percent of the

derivatives market was centrally cleared.”

According to the OCC, as of December 31, 2015 there were $237

trillion in notional derivatives (face amount) at the 25 largest bank

holding companies with the bulk of that amount on the books of the

insured banks. That compares with $169 trillion on the books of the 25

largest bank holding companies at December 31, 2007, just prior to the

implosions on Wall Street. This means there has been an explosive 40

percent increase in eight years when the Obama administration was

supposed to be reining in risk on Wall Street.When you hear Hillary Clinton repeatedly tell the public that she wants to continue along the same pathways as President Obama and that the restoration of the Glass-Steagall Act is not needed, let the image of Goldman Sachs Bank USA and its FDIC insurance logo and its $41 trillion in derivatives come to mind.

Four

Largest Banks by Derivatives — Percentage Ratio of Credit Exposure to

Risk-Based Capital: OCC Report Dated December 31, 2015

No comments:

Post a Comment