is Chief Analyst at Nordea Markets, a subsidiary of Nordea

Bank AB. Svendsen specialises in Emerging Markets research.>> Special to The BRICS Post

is Chief Analyst at Nordea Markets, a subsidiary of Nordea

Bank AB. Svendsen specialises in Emerging Markets research.>> Special to The BRICS Post

>> The BRICS face headwinds from the Russia/Ukraine crisis, the Chinese rebalancing and the approaching Fed tightening at a time when they are already challenged by weak growth and high inflation. Over the coming year, we believe success or failure will be determined by policy-makers’ ability to manoeuvre through these headwinds and that foreign exchange (FX) policy will play the most important role. For the BRICS to retain their claim of being the economic powers of the future, however, structural reforms are needed.

Headwinds

Three key risks darken the outlook for growth in the BRICS:

1) The Russia/Ukraine crisis has already taken its toll on growth in Russia and more sanctions or further escalation still cannot be ruled out.

2) Chinese growth will continue to slow as the economy is rebalanced. Authorities may have slowed the tightening just a bit during the summer and growth momentum has picked up in recent months, but we believe that tightening will resume once this year’s growth target has been secured.

3) Fed tightening is moving closer. When the US Federal Reserve says the first rate hike is imminent, we believe Emerging Markets will sell off at least to the same extent as in May/June last year, when the then Fed Chair Ben Bernanke said that tapering was imminent.

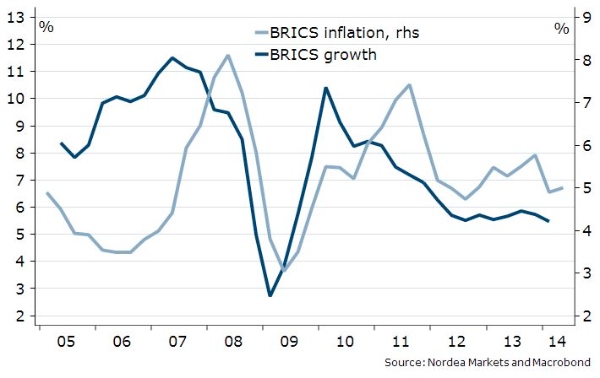

Growth is slow already

Policy-makers

in these five nations face numerous challenges to manoeuver through

these headwinds. Growth is slow already by historical standards,

inflation is at the high end of comfort zones in Brazil, Russia, India

and South Africa and a potential new round of Fed-related Emerging

Markets selloffs is a threat not only to growth and inflation but also

to financial stability.

Policy-makers

in these five nations face numerous challenges to manoeuver through

these headwinds. Growth is slow already by historical standards,

inflation is at the high end of comfort zones in Brazil, Russia, India

and South Africa and a potential new round of Fed-related Emerging

Markets selloffs is a threat not only to growth and inflation but also

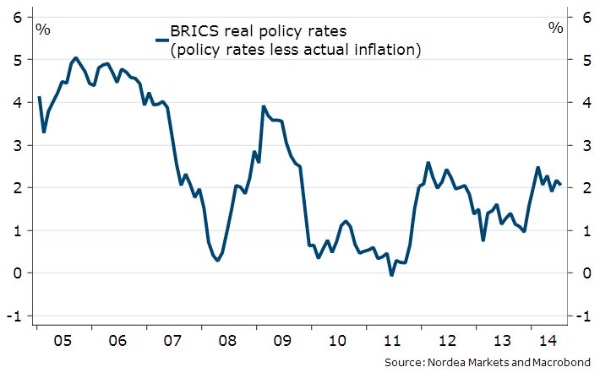

to financial stability.When the Russian central bank hiked its key policy rate by 50 bp in a surprise move at the end of July, it cited FX risks related to an escalation of the conflict with Ukraine and monetary developments abroad (read: Fed tightening) as key reasons.

The Brazilian, Indian and South African central banks have all hiked rates this year and risks remain skewed towards further tightening to fend off potential capital outflows and FX weakening going forward. Looking into next year and perhaps even 2016, we see little or no room to cut policy rates to revive growth.

FX policy is key

![Russian President Vladimir Putin, Prime Minister of India Narendra Modi, President of Brazil Dilma Rousseff, President of China Xi Jinping and President of South Africa Jacob Zuma at the 6th BRICS Summit in Brazil on 15 July 2014 [AP]](http://thebricspost.com/wp-content/uploads/2014/07/41d4f1586eb6e4bde771.jpg)

Russian

President Vladimir Putin, Prime Minister of India Narendra Modi,

President of Brazil Dilma Rousseff, President of China Xi Jinping and

President of South Africa Jacob Zuma at the 6th BRICS Summit in Brazil

on 15 July 2014 [AP]

Chinese authorities allowed the yuan (CNY) to weaken in the early part of this year. Admittedly, we believe the main reason was to curb hot money inflows, but it surely eased some of the pain from tight domestic policies as well. We still believe that a stronger CNY is needed to facilitate the gradual rebalancing of the economy, but temporary currency weakening is definitely a tool that can be deployed in future to give a short-term boost to growth momentum when needed.

The Russian ruble (RUB) weakened significantly in the first months of the year, prompting large FX interventions at the border of the corridor. Yet during the summer, the Russian central bank announced another move towards a free-floating RUB by the end of this year. The corridor was widened, interventions within the corridor were reduced, and the cumulative interventions needed to move the corridor were reduced too. These changes have probably been planned for a long time, but sticking to the plan at a time when FX risks are high clearly indicates that controlled FX weakening will be one of the first lines of defence going forward.

The Brazilian central bank has intervened heavily throughout the year to manage the Brazilian real (BRL). When the presidential elections are over in October, we believe there will be more room to allow for a weaker BRL if fiscal policy is tightened at the same time. Aécio Neves, a presidential candidate, recently called for a floating BRL to revive the economy.

In the longer term …

To retain the claim of being the economic powers of the future, structural reforms are needed. Once the BRICS were known for high growth and low inflation, but in recent years inflation has been high and growth low. There are some reasons to hope for reforms, though.

The new government in India has been elected on a strong reform agenda. Implementation is obviously the key, but at least significant increases in infrastructure investment are likely to be implemented.

In Brazil, the presidential race has re-opened and incumbent President Dilma Rousseff no longer looks like a clear winner. A new president would bring some hope of structural reforms.

The world’s biggest conventional gas producer, Russian Gazprom’s historical gas deal with China

will not only bring a massive increase in investment next year, but is

also an indication that Russia may finally be ready to use the

government’s oil wealth for investment and reforms.

The world’s biggest conventional gas producer, Russian Gazprom’s historical gas deal with China

will not only bring a massive increase in investment next year, but is

also an indication that Russia may finally be ready to use the

government’s oil wealth for investment and reforms.And last but not least, the recent announcement of a BRICS development bank suggests that structural reforms and growth-enhancing investment are high on the agenda in the BRICS after years of weak growth.

Skilled policy-makers will be required to manoeuvre through the headwinds over the coming year with controlled currency weakening likely to be a favoured option, while success or failure in the longer term will be determined by the BRICS countries’ willingness and ability to reform. Historically, most reforms seem to have been done back against the wall.

The views expressed in this article are the author's own and do not necessarily reflect the publisher's editorial policy.

HEADWINDS, the BRICS are headed into the headwinds of changing the world structure that was ruled via WESTERN money changers.

ReplyDelete